From the Edges to the Core: How Deleveraging Moves from Risk Assets into Credit

March 2nd, 2026

Financial stress usually does not start at the core of the system. It begins where risk taking is highest, in the most speculative and leveraged trades. Over the past month, high volatility risk assets have compressed, rate volatility has risen, and credit spreads have begun to widen modestly. Those are early signs of pressure building at the edges.

What to Take Away from This Week's Edition:

When speculative positions unwind, price swings increase and volatility rises. If that pressure continues, it can spread into credit markets. That is when borrowing becomes more expensive and lenders grow more cautious. Companies that rely on refinancing debt may face higher interest costs or reduced access to capital. To adjust, they may cut spending, delay expansion, or slow hiring. As financing tightens, growth loses momentum.

What begins as stress in the outer layers of the market can gradually move inward. If it reaches the center, it shifts from a market disturbance to a broader economic slowdown.

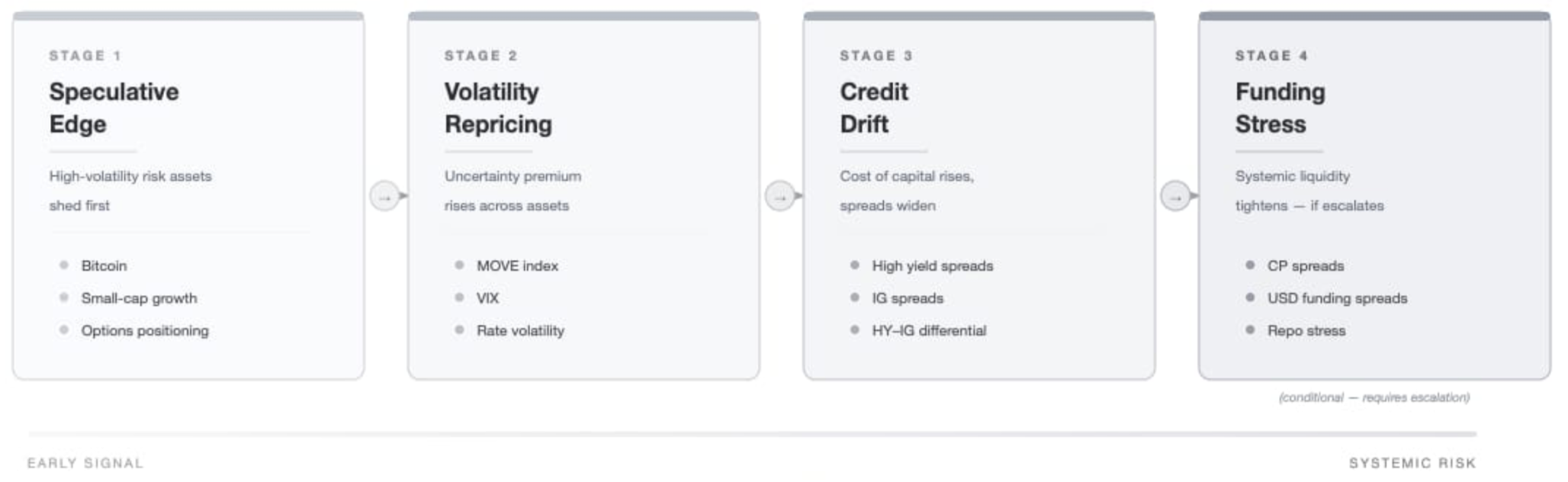

The Transmission Path of Deleveraging

Deleveraging does not appear all at once. It moves inward in stages, starting where risk is most concentrated, then works its way toward the core of the system.

The typical sequence looks like this:

Speculative risk assets compress.

Volatility reprices.

Credit spreads drift wider.

Funding markets tighten (if escalation occurs).

Not every episode progresses through all four stages. But when deleveraging becomes meaningful, it tends to follow this path.

This week, markets appear to be between stages two and three.

Stage One: Compression at the Edges

Bitcoin often reflects changes in speculative risk appetite before broader markets react because it is more exposed to changes in liquidity and sentiment than traditional assets.

BTC is down roughly 26% over the past 30 days — a meaningful compression at the speculative edge.

Equities, by contrast, are relatively stable. The S&P 500 is only modestly lower over the same period, and market breadth has remained steady. This divergence is important to understand..

When deleveraging begins, it usually shows up first in the highest-volatility exposures. That appears to be the case now.

This is a narrowing of risk tolerance at the margin.

Bitcoin’s move tells us that appetite for high-volatility exposure has cooled. Equities have not followed in kind -meaning speculative compressing is still selective and has not yet reached systemic levels.

Stage Two: Volatility Repricing

While equities have held relatively firm, rate volatility has not. The MOVE Index has risen materially over the past month. MOVE measures volatility in the Treasury market — effectively the price of uncertainty around interest rates.

Rising rate volatility signals uncertainty about where policy is headed and how the macro outlook will unfold. It means investors are less confident about the path of interest rates and growth.

Even if asset prices look calm on the surface, higher volatility changes behavior. Hedging becomes more expensive. Investors reduce position size. Conviction weakens because the range of possible outcomes feels wider.

When volatility resets higher, financial conditions tighten in subtle ways. Capital becomes more cautious. Risk taking slows, even without a dramatic selloff.

That appears to be where we are now.

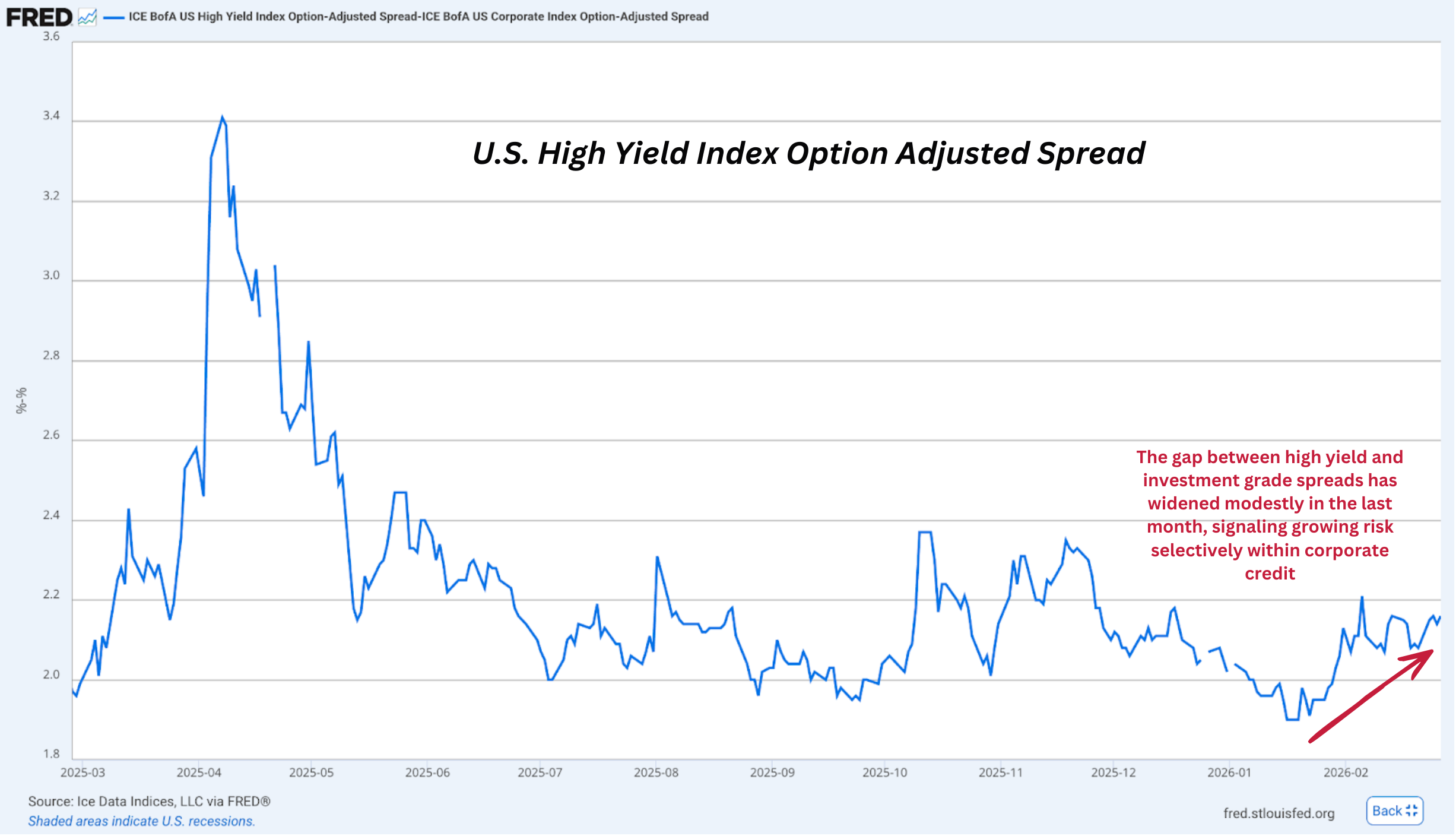

Stage Three: Risk Discrimination Begins in Credit

Over the past month, high yield spreads have widened more than investment grade spreads. The gap between the two has increased by roughly 18 basis points.

When deleveraging begins to move inward, lower-quality borrowers tend to reprice first. Investors demand additional compensation for weaker balance sheets before they reprice stronger issuers.

The widening gap between high yield and investment grade spreads is not a crisis signal. But it is a signal of growing selectivity. Capital is becoming more cautious.

That is how early-stage credit drift typically appears.

What Has Not Happened

Importantly:

Commercial paper spreads remain stable.

SOFR and short-term funding rates are steady.

The USD is not surging.

Repo facilities are not signaling strain.

The system’s plumbing is holding steady. That distinction matters.

Deleveraging at the edges does not automatically become systemic. It must move through credit and into funding to become something larger.

We are not there.

Hard Value and Positioning

Gold has risen roughly 3% over the past week and nearly 2% over the past month.

That is not explosive, but it is steady.

In an environment where volatility is elevated and credit is drifting, capital often rotates toward monetary durability rather than speculative upside. Gold’s behavior fits that pattern.

Again, this is caution - not crisis.

What Would Signal Escalation

To move from credit drift to broader stress, we would need to see:

High yield spreads widen materially beyond current levels.

Repo facility usage surge meaningfully.

Equity breadth deteriorate sharply.

Until those conditions appear, the progression remains contained.

The Larger Lesson

Deleveraging rarely announces itself with a headline.

It begins quietly - with compression at the edges.

It moves through volatility.

It shows up gradually in credit.

Only later, if at all, does it challenge funding markets.

This week’s data suggests we are between volatility repricing and early credit drift.

Measured. Not dramatic. But worth watching.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.